Food Inflation Tailrisks

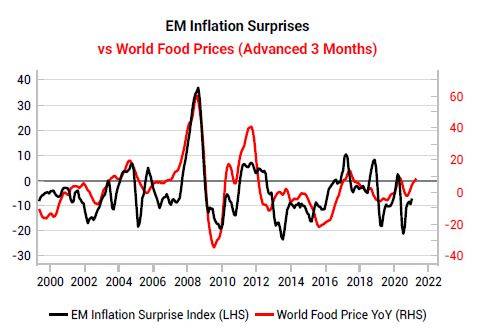

Food prices are correlated with EM inflation surprises. The current surge in soft grain prices should be monitored in case it spills over into general inflation expectations.

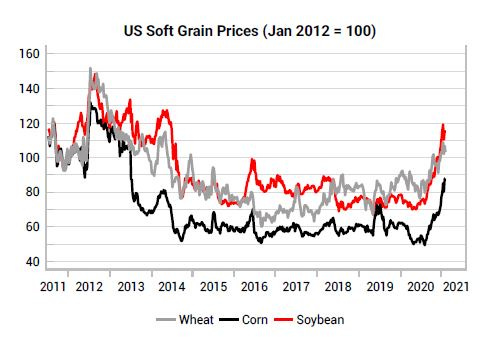

Food inflation can have outsized impacts on inflation expectations due to the higher frequency at which consumers buy food. In the US, food and beverage directly accounts for about one sixth of the CPI basket by weight, but in many EM countries, the weighting is in the range of 30-50%.The current surge in soft-grain prices is something to be aware of as a medium-term risk to inflation expectations, especially in EM. (High food prices have been cited as one of the catalysts for the Arab Spring uprisings back in the 2010-2012.)

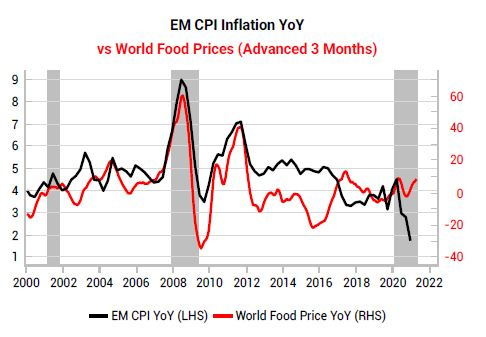

Historically, we can see a close correlation between world food prices and EM inflation surprises.

Due to the lockdown recession, the underlying resilience of food inflation is being masked, with a notable divergence between EM CPI and food prices at present. The concern is that later in 2021, as global economies recover and re-open, the EM inflation picture could change rapidly as cyclical inflation comes on top of food inflation.

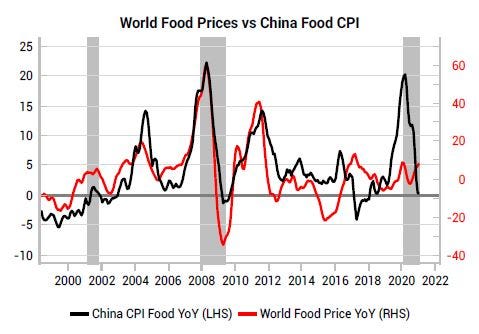

We are also tracking Chinese food prices closely in case food inflation there spills over into global food prices. Historically, China’s food CPI and global food CPI have been closely correlated, but the relationship has broken down in recent years due to China’s struggle to contain African Swine Flu, which has caused huge moves in pork and meat prices. The combination of coronavirus disruptions and African Swine Flu drove China’s food CPI to 20% during the depths of their pandemic.

EM food inflation risks are now becoming more visible for 2H21 and may restrain EM central-bank policies later in the year.