Inflation Outliers - Excerpt from VP September DM Leading Indicator Watch

This post is an excerpt from our Sept 22nd report to Variant Perception (VP) clients (link to original report), digging into lesser-followed country-specific themes across DMs.

United Kingdom: Disinflation comes through

The BoE paused rate hikes in September as more disinflationary signs came through.

We had previously been fading the hawkish BoE theme with short GBPAUD and Sonia vs Euribor trades.

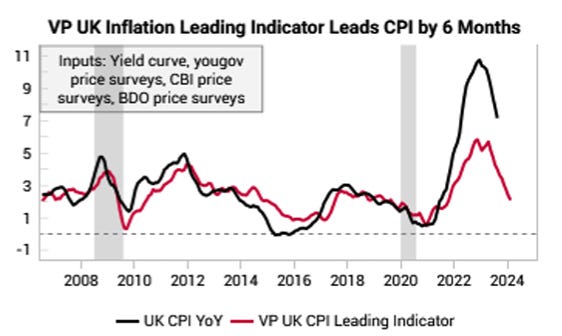

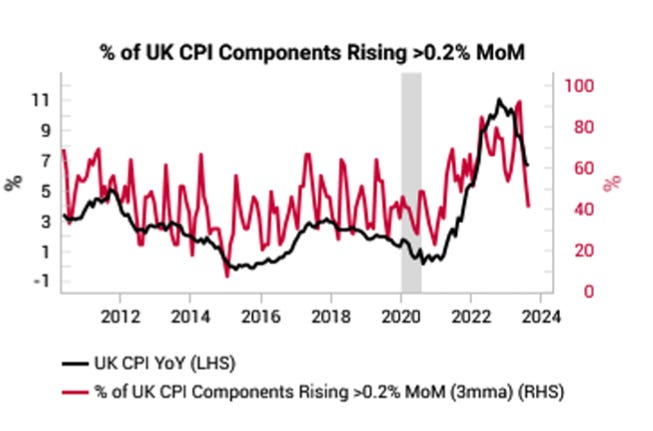

Our UK inflation leading indicator continues to fall, confirming the cyclical disinflationary trend. The proportion of CPI components rising +0.2% MoM has also collapsed.

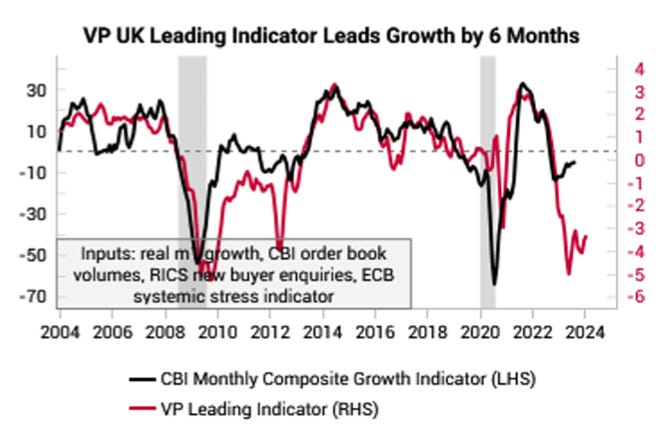

The UK economy is likely already in recession.

The UK economy is also more vulnerable to rate hikes as mortgages are typically only fixed for 2 or 5 years, creating a steady headwind to the consumer.

Norway: Managing Inflation Amidst NOK Dynamics

Persistent NOK weakness and strong labor markets are driving up our Norway inflation leading indicator (an outlier within G10).

This is corroborated by various inflation-linked surveys. Salary expectations are still trending higher for both households and businesses, as is expected inflation.

Since much of the inflationary pressure is derived from NOK depreciation, Norges Bank could feel pressure to address the inflationary outlook by tilting its FX purchase policy. As the current account surplus rises, Norges banks buy more foreign currency (i.e., sells more NOK).

Norway’s massive oil revenues and sovereign wealth fund have an outsized effect on the NOK as foreign investments are hedged into NOK. One can proxy for this FX hedging flow by tracking Norges Banks’ monthly FX sales or purchases each month.

A slower pace of NOK sales or a pause could have an outsized impact on NOK crosses and allow some catchup appreciation. The bottom chart shows that EURNOK and the NOK NEER are starting to mean-revert from 5y extremes.

Japan: Tackling Elevated Inflation with Strategic Pivots

Our Japan inflation LEI is still being propped up by elevated inflation surveys.

On the anecdotal front, there has been a slew of price increases:

1) Japan Rail Pass increasing +60% in October

2) Tokyo Disneyland highest ticket prices in 40 years

3) Japan gasoline prices hit record high.

Our long Japanese insurance position is coming good on the more hawkish BoJ headlines (link) and remains the asymmetric way to position for a higher rate regime.

Our Japanese growth LEI is also bottoming and turning up, adding further fuel to the narrative on the BoJ’s need for a hawkish pivot.

While our BOJ hiking regime indicator flipped to the hawkish regime in August, the BoJ will need to abandon Yield Curve Control (YCC) completely to get out of its impossible trinity problem.

Unless the BoJ does something dramatic, the FX carry trades funded by the JPY will likely continue to do well given the large margin of safety embedded in rate differentials vs Japan’s still-negative overnight rates.

For a comprehensive insight into our investment framework, visit