Leaning into the 1969-70 roadmap

The below is an excerpt from our March 1st report.

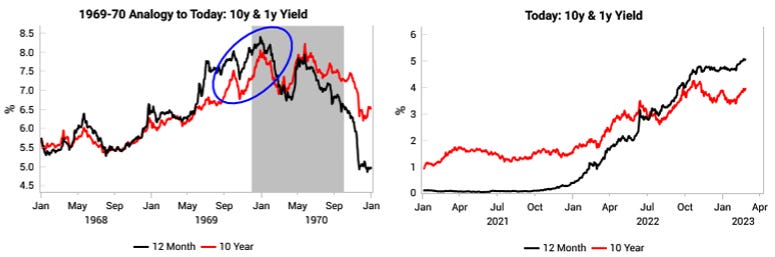

There are many parallels between today’s macro landscape and the period heading into the 1969-70 US recession:

Previous massive fiscal stimulus that propelled inflation (Great Society, Vietnam War vs Covid stimulus)

The Fed flip into inflation-fighting mode with persistent hikes

Collapsing leading growth indicators

High inflation but not an obvious rollover

15%+ equity drawdown from the peak

Surging yields and inverted yield curves

Very tight labor markets

The 1969-70 recession was mild and took a while to impact inflation. Inflation plateued at a high level throughout the recession.

The yield curve bull steepened, but yields took a while to fall in absolute terms.

The start of that recession marketed the top in yields and the recession drove a final leg lower in equities. The equity market recovered very quickly from the final leg lower.

The key takeaways for today:

VP’s inflation LEIs suggest more downside risk to inflation today vs 1969-70, which supports long fixed income positions.

This also supports curve steepening, though timing is key for steepeners as negative carry can hurt levered players. 2s10s forwards have fallen sharply. The at-the-money (convexity-adjusted) forward levels on yield curve caps are now much lower making tail-trades on curve steepening attractive.

The Fed has never finished its hiking cycle until the real policy rate goes positive. We are still on pace for this to occur by May 2023.

Get the full picture at variantperception.com