Macro tailwinds persist + what to use as early warning indicators

Weekly Wrap, Oct 3, 2025

Variant Perception, Made Repeatable.

Rigorous investment research grounded in auditable quantitative models. No black boxes, no guru calls.

Research

Macro tailwinds persist + what to use as early warning indicators - Oct. Macro Snapshot

LEIs for growth, liquidity, and policy remain supportive of 6m fwd outlook for risk assets. The incremental positive since last month: Eurozone and China growth LEIs have risen further.

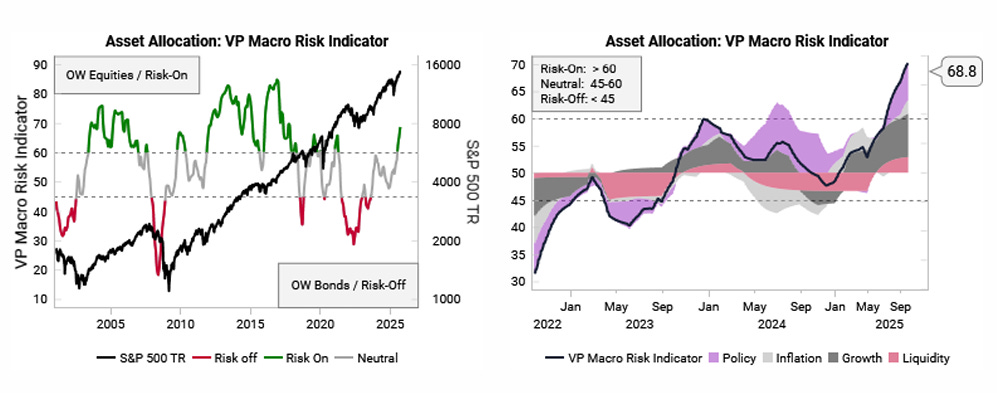

Macro backdrop remains good. However, many asset classes have low embedded risk premia and high valuations relative to history.

We flag two early warning signs to indicate when high valuation assets are vulnerable:

A) VP Correction Signal; and

B) any signs of bear steepening, especially in response to further Fed cuts.

Our N. American semiconductor capital cycle score remains healthy and better than tech hardware and software. Scores are also much better than European/Asian semis.

Notes

Cyclical Asset Allocation: “Risk-on” tailwinds persist, potential for equity rally to broaden out

Fed Easing Cycle: Tracking “no recession” Fed easing cycles so far

US Inflation: Inflation remains above target, but leading indicators are rolling over

Early Warning Signs: Keep calm, watch VP Correction Signal / bear steepening for warning signs

Capital Cycle: Semis still capital scarce vs tech hardware/software, US better than Europe/Asia

Equity: Earnings optimism elevated, macro tailwinds for EM, small caps

Fixed Income: Yields trading near low end of fair value range, moderately biased upwards

FX: Cyclical FX Edge model still points to USD rebound

Commodities: Commodity outlook improving, energy and metals cheap in gold terms