Post-Iran Stabilization - EM/DM Leading Indicator Watch

Weekly Wrap - 27 June 2026

This week's charts and research highlights from Variant Perception.

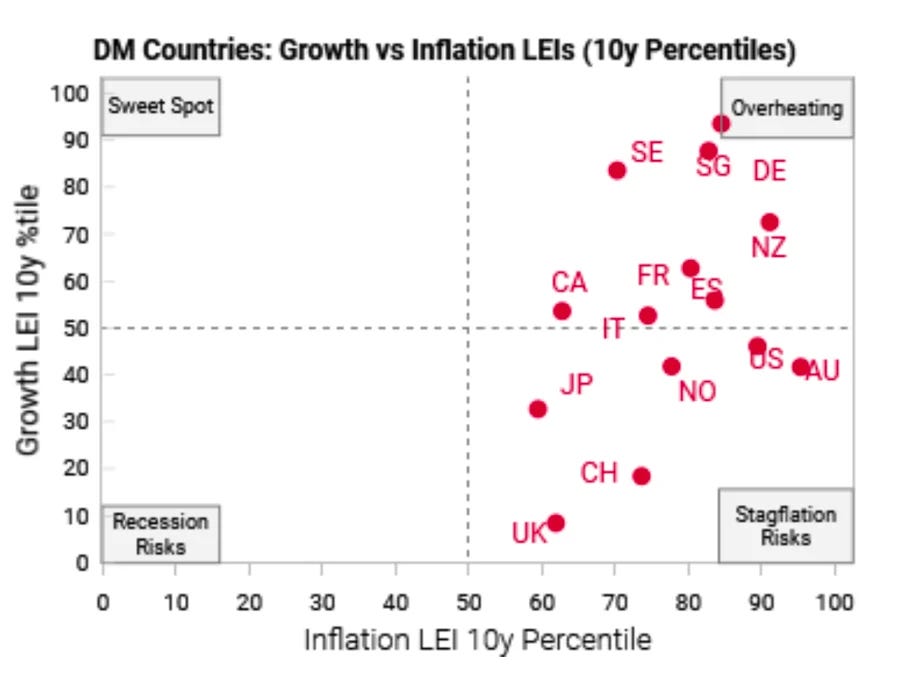

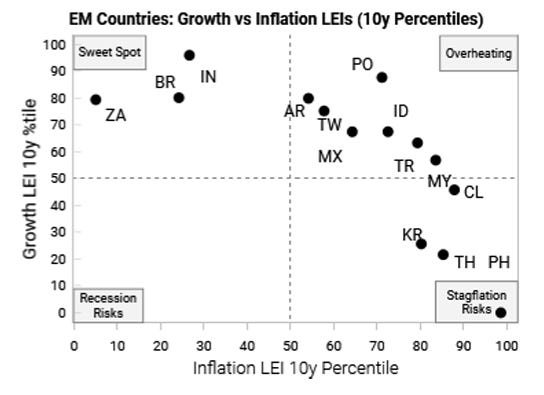

Chart of the Week

There remains meaningful dispersion across different economies. DM: both UK and Switz continue to have poor growth LEIs, helping our GBP receiver and short CHFJPY.

Post-Iran Stabilization - EM/DM Leading Indicator Watch - Jun 25

The de-escalation of the Iran conflict has successfully arrested the downside momentum in global growth data and the upward momentum in inflation data.

Within DM, UK growth risks are more recognized and we take profit on our GBP receivers. We stick with short CHF vs long JPY as BoJ policy is at a breaking point. We shift our short EUR vs long USD into a short EUR vs long AUD given the AUD sell-off.

Within EM, our Brazil risk-parity position is exposed to election risks and we would look to reduce exposure in the coming weeks. In S. Korea there are signs the Semi/AI boom is relatively narrow and not yet helping other parts of the economy. Indonesia is seeing a large cluster of LPPL crash exhaustion buy signals.

Post-Iran Stabilization - June EM/DM Leading Indicator Watch - [Video Discussion]

Speakers: Tian Yang (CEO & Head of Research) & Hugh Vuillier (Head of Client Relations)

DM

UK: Yields at 3-month lows, now more aligned with macro view => take profit on receivers

Japan: BoJ still at breaking point in face of fiscal & inflation => stick with short CHF vs long JPY

Australia: Growth peaking, but hedging demand for AUD remains => short EUR vs long AUD

Canada: Resilient growth LEIs, any USMCA-induced CAD sell-off is a buying opportunity

EM

Brazil: Political/fiscal risks overwhelming cheap valuations into October elections

S. Korea: Semi/AI drives growth, but BoK’s hawkishness already well priced

India: Low monsoon rainfall remains the tail risk, not yet time to buy Indian assets

Indonesia: Equity capitulation likely complete on LPPL signal, MSCI delay and rate hikes

Trial our Research?