The "bad" kind of rate rise

The speed of the surge in real yields over the past month is now comparable to the Taper Tantrum (left chart), and when we decompose the yield surge, it has been driven mostly by rate expectations rather than by term premium (right chart).

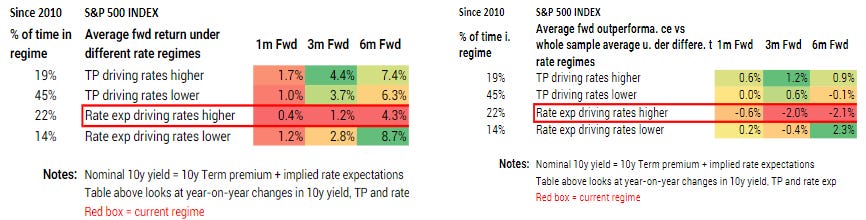

This is the “bad” kind of rate rise and puts us into a regime of lower equity returns. We have split up the period since 2010 (when the Fed started impacting term premium) into different regimes based on whether rates are rising or falling and whether it is mainly rate expectations or term premium that is driving the change. In absolute terms the S&P has on average risen in each regime (left chart below, unsurprising given the uptrend in the S&P since 2010), however if we compare the S&P returns vs its own historical average over the whole sample (right chart below), we note that the current regime of rate expectations driving rates higher tends to see below average S&P returns.

Higher rates driven by anticipation of hawkish monetary policy (instead of hopes for growth or reflation) tend to be the worst regime for equity returns. The “good” kind of rate rise is when it is mainly driven by higher term premiums, reflecting better sentiment towards reflation and growth (i.e. the regime we saw for most of 2021). We turned more cautious on equities after the March Fed meeting suggesting investors switch towards a “sell rallies” mindset. The developments over the past few weeks further reinforce that cautious view. As a quick reminder, our cautious equity view is primarily driven by our LEIs that point to poor liquidity conditions and a lack of China reflation.

To get a sense of how factors and sectors perform within the current rate regime, we look at outperformance of each factor or sector relative to its own average performance over the whole period since 2010.

The left chart above shows that all sectors tend to experience lower returns than average when rate expectations are driving rates higher, but the more defensive sectors like utilities and healthcare have generally held up better.

Consumer stocks and communication services are most exposed. In terms of equity factors (right chart above), profitability and size tend to perform the best (i.e. higher quality and larger companies), while leverage and volatility should be avoided.

Get the full picture at variantperception.com