Thoughts on Quantifying Equity Crowding + Not too hot, Not too cold (G3 LIW)

Weekly Wrap - 10 July 2026

This week's charts and research highlights from Variant Perception.

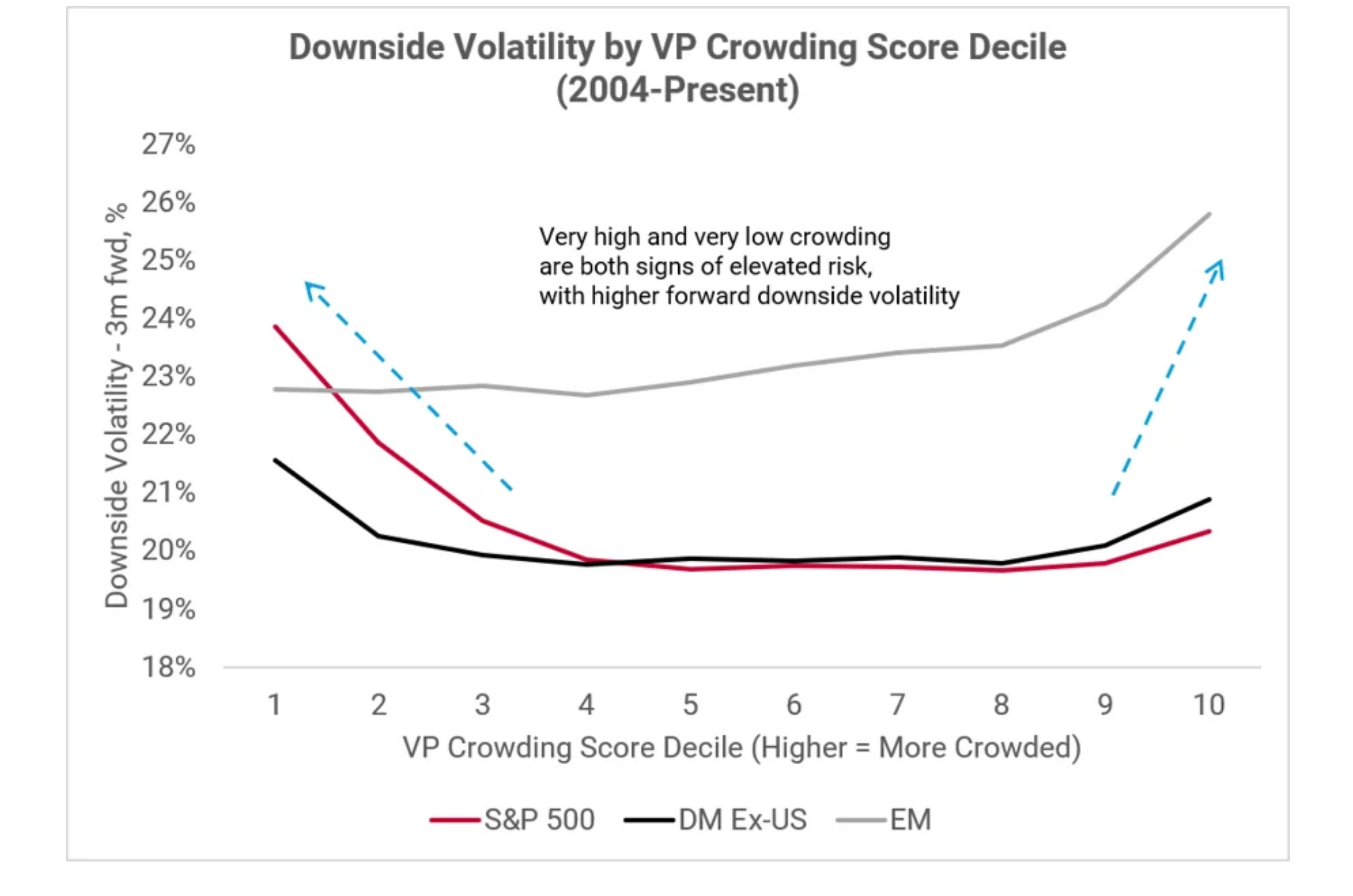

Chart of the Week

Stocks with both very high and very low crowding scores show significantly higher forward downside volatility. Investors should aim to stay in the sweet spot for crowding to maximize portfolio resilience.

Thoughts on Quantifying Equity Crowding - July 8

The basic mechanics of crowding are straightforward: when a stock is widely owned, universally recommended by sell-side analysts, and actively chased by short-term traders, its shareholder base becomes inherently fragile.

Asymmetry: Crowded stocks suffer from asymmetric returns. They benefit less from good news (which is already priced in) and suffer disproportionately on bad news.

Risk Management: Crowding is primarily a risk management mechanism rather than a pure alpha generator. Being contrarian for contrarian’s sake is unprofitable. Instead, tracking crowding allows investors to build portfolio resilience and mitigate catastrophic tail-risk around events.

Portfolio Construction: It is best to avoid stocks at both extremes (very high and very low crowding). While extremely high crowding exposes you to big drawdowns, extremely low crowding often signals structural problems hidden from standard accounting disclosures.

[Video Discussion]

Not too hot, not too cold - July G3 LIW

Speakers: Tian Yang (CEO & Head of Research) & Hugh Vuillier (Head of Client Relations)

Not too hot, not too cold - G3 Leading Indicator Watch - July 10

US growth looks set to remain at trend, while US inflation fears are overstated, as core inflation is capped by subdued housing, the K-shaped consumer and muted activity across small businesses.

Chinese domestic demand remains weak as the economy remains geared towards exports and sovereign-aligned investment. Repatriation flows are providing a tailwind for the RMB, overcoming the negative carry vs the USD.

Our eurozone growth LEI is still rolling over, but the pace of deterioration has moderated. The fallout from the Iran conflict has been relatively contained so far, with a notable rebound in the ZEW and Sentix expectation surveys.

US

Growth: Outlook steady, despite some noise around GDPNow estimates

Consumer: K-shaped consumer & negative real income growth cap inflation upside

Labor: Still not inflationary, not recessionary

Inflation: Subdued core inflation LEI vs surging headline CPI

China

Economy: Muted growth as domestic demand remains weak

FX: RMB breadth remains very strong, flow tailwinds still intact

Eurozone

Growth: Marginal improvement in leading data, growth outlook stabilizing at lower levels

Inflation: Upside risks to service inflation could force the ECB to maintain hawkish stance

Trial our Research?