US Election Cycles

"Change" elections reverse market leadership

This post is an excerpt from our February 28, 2024 When Election Risks Matter for Investors thematic report to VP clients. The full length, original report can be viewed here. To gain access to more of our research, contact us here.

US elections as “referendums on the past”

We expand upon our previous work on the Keys to the White House 2024 based on historian Allan Lichtman's US election framework.

Lichtman's study of historical elections suggests one should de-personalize the candidates and view elections as “referendums on the past”, with voters deciding on “continuation” or “change”:

“Voters can be happy with the past four years and want a continuation of the status quo (favoring the incumbent party). Voters can also be unhappy with the past four years and simply want change - irrespective of the type of change - which would favor the challenging party.”

Given the nature of the US's two-party system, the public's desire for continuation or change of the status quo is well represented by the shifts (or not) in the party of the elected president relative to his predecessor.

In the below table, we categorize each US presidential election since 1972 as either a "continuation" or "change" election, contingent upon a change in political party from the prior president.

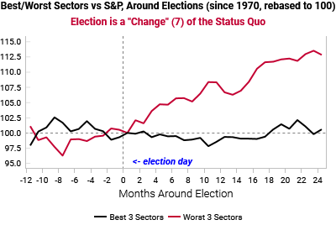

Changes in political leadership lead to changes in market leadership

Change elections tend to bring economic uncertainty, causing investors to anticipate policy changes and their effects on corporate profitability.

Sector leaders from the previous political era are often the greatest beneficiaries from policies that the newly elected party may want to change. Correspondingly, policy headwinds that have created sector laggards now have the potential to be removed

This explains why changes in political leadership historically lead to changes in market leadership, with the three worst performing sectors in the calendar year leading up to a “change” election outperforming in the next 2 years.

After continuation elections, sector leadership tends to remain consistent, as the re-elected party is unlikely to change policies that favor the same industries.

Case study: Reagan & Clinton initial vs re-election

Looking at a few more well know political episodes helps paint an even clearer picture.

In the 1980 US presidential election, widespread dissatisfaction and the perceived ineffectiveness of the Carter administrations ability to handle economic stagflation propelled Ronald Reagan to victory. Sector laggards proceeded to outperform prior leaders by nearly 70% the next two years.

The opposite was true following Reagan's landslide “continuation” victory in 1984, with prior sector leaders continuing to outperform.

Clinton's denial of George H. W. Bush's second term ("it's the economy, stupid") led to a sharp reversal in sector leaders, in contrast to Clinton’s relatively uncontested re-election in 1996.

Case study: Obama’s “change” campaign, G.H.W. Bush post Reagan

Obama's self-described “change” campaign shows a similar reversal pattern in sector leadership around the 2008 election, although the GFC was obviously a major event that also drove changes in market leadership.

George H.W. Bush's election following two Republican terms under Reagan shows continuation of sector leadership is not only a result of an incumbent re-election but from a continuation of the same party.

Change elections are catalysts for the capital cycle

Political policies are natural catalysts for over or underinvestment in a given industry.

Capital scarce industries outperform even more following change elections as sector specific capital restrictions potentially ease.

Returning to 2008, capital scarce sectors such as Health Care greatly outperformed (below left chart) with added benefit from novel legislation like the Affordable Care Act (Obamacare).

Meanwhile, the Bush administration's continued focus in the Middle East throughout his second term led to minimal shifts in policy.

In our recent November Macro Snapshot report, Of Elections and Term Premium, we dive deeper into the implications of the coming week’s US election. To gain access to more of our research, including our Macro Snapshot and full-length election risk thematic report, contact us here.