US inflation: not fully out of the woods yet

This is a Note originally shared with VP clients on January 7, 2025. The original Note can be viewed here. To gain access to more of our research, contact us here.

The various inflation indicators we track shows moderate upside risks to inflation. This will limit the Fed's ability to cut interest rates, but these inflationary pressures do NOT yet look high enough to force hikes.

Our US inflation leading indicator still shows inflation settling above target with a 6-month forward point estimate of 3.5% YoY. It is also notable that we are starting to see a rebound in various price surveys, such as the recent rise in the NFIB price plans and compensation plans.

Globally, the breadth of inflation is also picking up again. The diffusion of all the raw input data into our inflation models is rising again. Inflation surprises are also rising again in more regions.

The regional Fed manufacturing surveys are showing a notable pick up in future price expectations, for both prices paid and prices received.

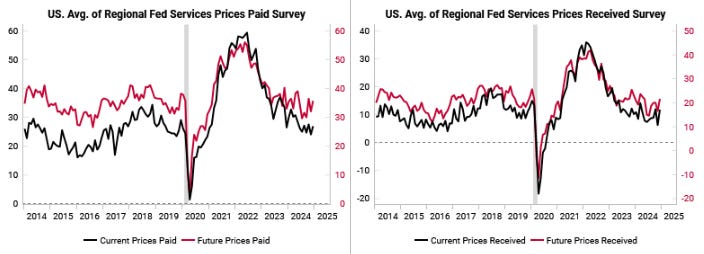

The regional Fed services surveys are showing a less dramatic uptick in price expectations, but these also look to be bottoming.

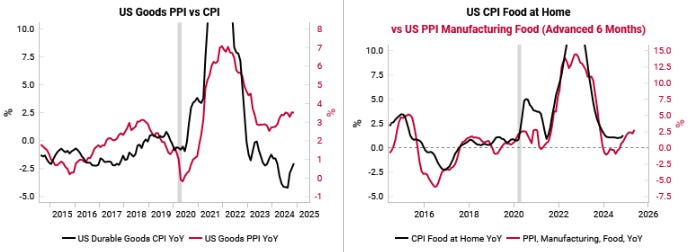

It is notable that the US goods PPI and food PPI are both trending higher, indicative of some cost pressures.

In summary, moderate upside risks to inflation mean we are skeptical that the Fed will be able to cut rates by much this year without a major recessionary shock (not visible in leading indicators at present).

Our new chart collections feature on the VP portal lets you easily see all the indicators we are tracking, including the above US inflation charts. To gain access to all our chart collections, contact us here.

I agree, no rate cuts coming at all this year. In fact, hikes are not impossible by the end of 2025