US sovereign risk distorting the message from credit spreads

Weekly Wrap, Aug 29

Variant Perception, Made Repeatable.

Rigorous investment research grounded in auditable quantitative models. No black boxes, no guru calls.

Weekly Wrap - Aug 29, 2025

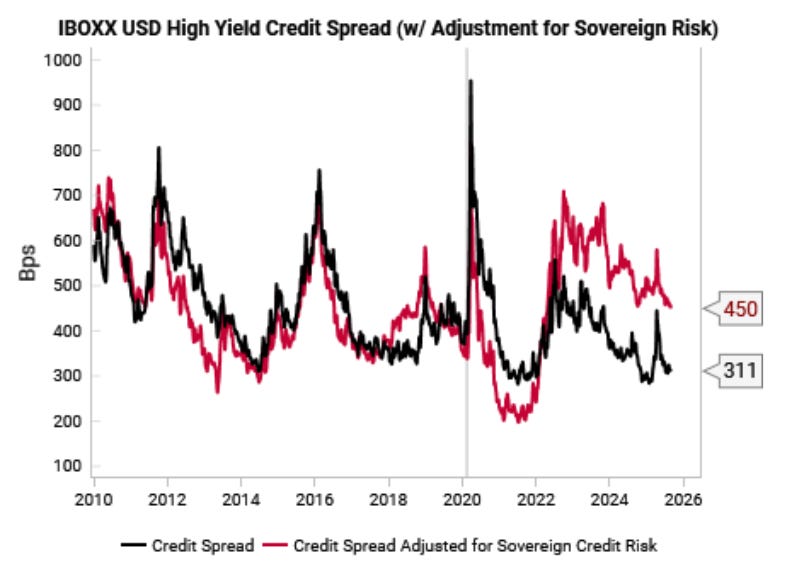

US sovereign risk distorting the message from credit spread

Credit spreads compressed by rising US sovereign risk premia pushing up the “risk free" Treasury yield.

Adjusting for sovereign risks, high yield credit spreads just at post-GFC averages.

Rather than prematurely reducing credit exposure, we think it is more effective to:

Hedge credit exposure via long March 2026 SOFR (bet on more Fed cuts); and/or

Long TLT puts (take advantage of falling volatility).

What We Got Right and Wrong (2Q25)

RIGHT:

Higher volatility around tariffs, a pivot to a US dollar downtrend, and continued housing weakness

Bullish calls for equities in China, India, and Brazil. Right in calls for US rates biased lower and most Q2 FX ideas.

WRONG:

Volatility around Liberation Day threw off our timing on the exhaustion of the gold rally and our bullish stance on industrial metals equities.

Lack of major repatriation flows meant our expectation for a yen rally was short lived, while global factors outweighed domestic ones in our call for the JGB curve to flatten.