VP's EM bottom fishing checklist (part 1)

Lessons from history

In this short series, we highlight how we combine our various frameworks and models to invest in EM, and signal the key signposts to start aggressively buying. The below is an excerpt from our March 30th report to VP clients.

Buying EMs after a crisis can be the trade of a lifetime; the key is “disciplined entry” to avoid holding cheap assets that get a lot cheaper.

We identify key signposts that flag the end of an EM crisis and an equity market bottom. Many EMs have already seen significant currency depreciation, and some frontier countries are in the midst of full blown crisis.

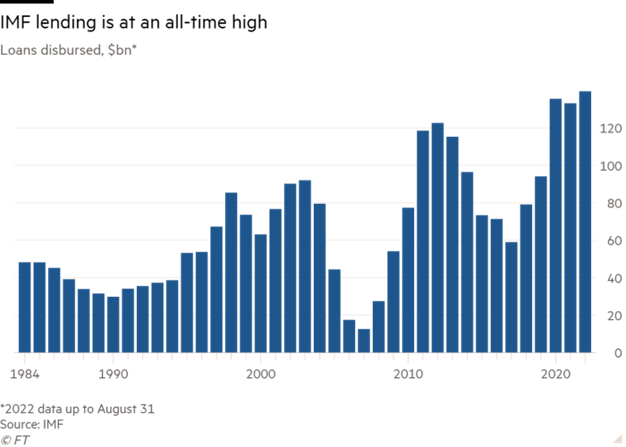

Bloomberg headline, Feb 12th 2023

Our June 2022 thematic report showed how we identify crisis candidates using current account deficits, M2/FX reserves, import cover and debt build-up.

In that report we also noted the need for patience to allow the crisis to play out before buying aggressively:

“The moves around devaluation events are so large that traditional technical measures are not too useful… The buy and hold returns after a devaluation show huge variation.”

“Renewed capital inflows into crisis countries indicate that the economic outlook has turned positive. As these inflows accelerate, equities and currencies can then reverse their crisis losses more quickly.”

“All happy families are alike; each unhappy family is unhappy in its own way.” – from Tolstoy’s Anna Karenina

The pace of recovery from crises varies widely, but what they all have in common is a monetary/liquidity upturn that fuels the recovery.

Renewed capital inflows into crisis countries indicate that the economic outlook has turned positive.

Asia 1997: FX reserves bottomed and marked an interim low in Dec 1997. But the final low in South Korea came many months after. An upturn in real M1 helped to call the bottom.

Mexico 1994: FX reserves bottoming and rising marked the low. Real M1 bottomed with the equity market, but didn’t turn up for a while.

Get the full picture at variantperception.com