Yield curve inversion: not an actionable investment signal

The below is an excerpt from one our recent reports, helping clients understand what a yield curve inversion means for their portfolios.

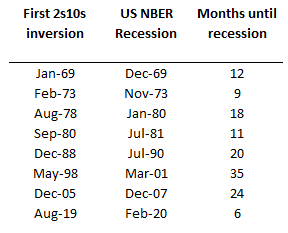

The yield curve has a good track record for predicting recessions, but its long and variable lead time make it a bad signal for shifting portfolio risk.

Negative term premium makes it easier for the yield curve to invert and further dulls its use as an actionable signal. Once the Fed actively reuces its balance sheet, term premium can start rising (helping the curve to re-steepen).

Powell has already pushed back on 2s10s as an indicator, pointing to 3m18m as a more reliable signal. Equities and commodities behavior after the first inversion is very mixed.

Our recession signal is designed to consistently trigger 3-4 months ahead of a recession - when equities typically peak. Our recession signal aims to capture stress in many parts of the market and economy.

Get the full picture at variantperception.com